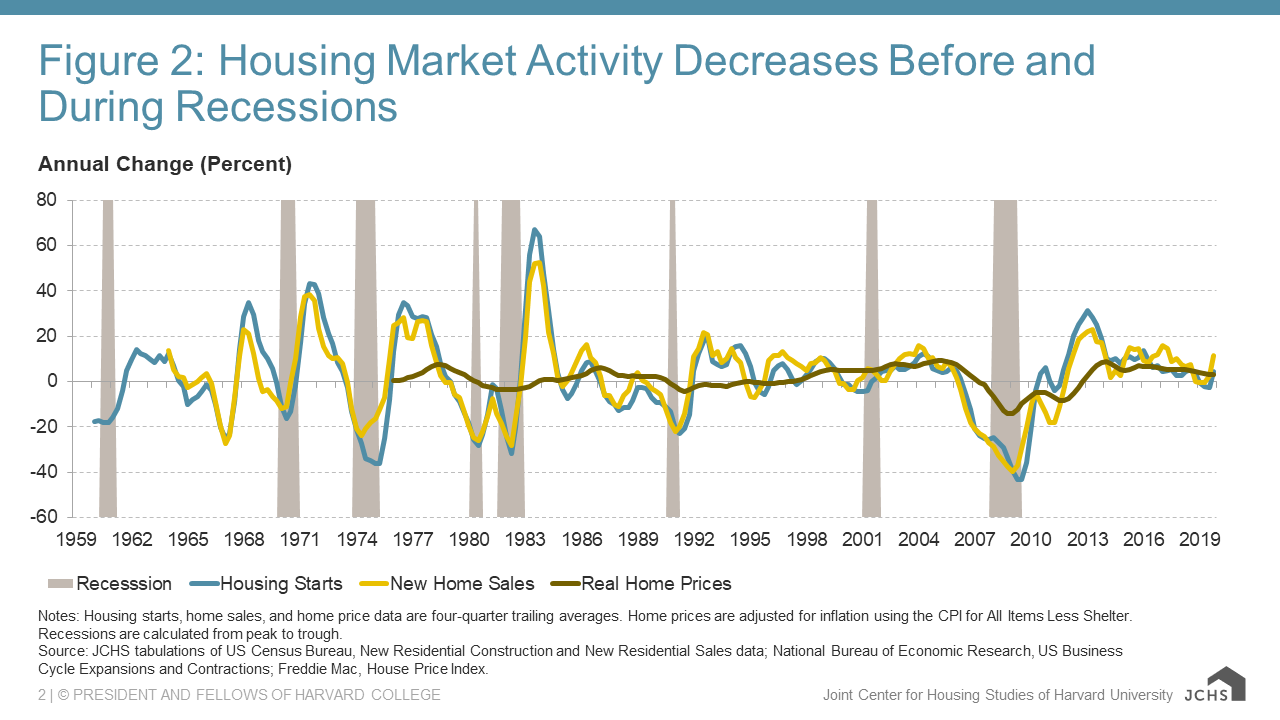

The July 2022 housing stats are in, and it’s official: the Nashville market is cooling off, though perhaps not in the way you were expecting. The number of transactions dipped by 19% in July when compared to the same time last year. We also saw a 76% increase in available inventory. You might think that greater availability and less demand would cause prices to fall, but so far, values are holding up.

This sudden change is all about the mortgage interest rates. The increased rates have caused many homebuyers to step onto the sidelines, at least for now, citing affordability and a potential downturn or recession. We’ve all been spoiled by the crazy low rates we’ve seen for the past few years. 2-3% rates don’t occur naturally in the market. The Fed put its thumb on the scale way back during the Great Recession by buying up mortgage-backed securities and then zeroing out the prime rate. The benchmark federal funds rate stayed artificially low for years. Too many years, because it fueled the recent price boom during Covid and the Great Resignation. Now we are in a situation where sellers are fearing that they’ve missed the boat, and many buyers are hedging on all fronts.

Still, the values are holding. This is because the price gains weren’t a bubble. The people purchasing during the last few years were well-positioned to do so. In many ways, the normalizing of the market is good for buyers and sellers. Suddenly buyers have more options and more negotiating power. And sellers are still able to capitalize on recent market gains.

What to expect when selling a Nashville area home today

Pricing is paramount. Smart pricing is always a good strategy no matter the market, but today it matters more than ever. A few months ago, agents were taking listings that were overpriced and still selling them, often with a premium beyond appraiseable value. Sellers also benefited from buyers having such little leverage that they couldn’t ask for a single concession. Some buyers were foregoing inspections or offering to take the property without negotiating for repairs. Buyers were footing the bill for title insurance. Buyers all but stopped asking for third-party home warranties. Today’s sellers are realizing that some concessions will likely be a part of the deal. Also, the days-on-market number is bound to increase. Selling in one weekend with multiple offers over the asking price will still happen to some belle-of-the-ball homes, but it will no longer be the norm.

Sellers should ready their home for market by consulting with their agent and/or their staging pro to get their property shining. They’ll need to study the comparables closely and set a down-to-earth, appraiseable price that compels the buyer to act.

What to expect as a home buyer in Nashville today

The good news is that you have some leverage for the first time in recent memory. The bad news is that interest rates are likely never going to be as low as they were a year or two ago. The Fed is still attempting to tamp down inflation, and one of its main tools is fidgeting with the rates. While the federal fund’s rate isn’t directly tied to mortgage rates, they do increase a bank’s borrowing costs, so the increase is offset to consumers down the line in the form of consumer rates and closing costs.

There are a few strategies to help alleviate some of the rising loan costs. The first thing you’ll want to do is consider how long you plan to own the property. If you only intend to stay for a few years, consider an Adjustable-Rate Mortgage. A 5 or 7-year ARM can offer an introductory rate that is more attractive than the long-term 15 or 30-year fixed rate mortgages.

The folks at Steadfast Mortgage have recently introduced a new program called Date The Rate, Marry The House. They are offering a program where you can refinance for free down the line if rates fall.

Wait for the perfect home, not the perfect rate. There’s always the opportunity to refinance at a better rate once you’re already in the home of your dreams.

Another opportunity lies in purchasing points. You, a builder, or the seller can contribute towards buying your rate down.

What’s coming next?

Of course, I don’t have a crystal ball, but I fully expect another Fed rate increase in the fall, probably by 0.75%. It’s important to put today’s rates into perspective. In the 1980s, some people paid 18% interest. In 2020, some people paid 2% interest. The historical average is just under 6%, so today’s really rates aren’t that scary. 6.75% is what I paid when I purchased my first home with a co-signed FHA loan in 2001. I was 25 years old, and it eventually led me into a fruitful career.

I believe that home price growth will flatten considerably, especially compared to recent years, but I don’t believe it will go backward. Even if we eventually decide to classify this time as an actual recession, it’s unlikely that values will go down much, if at all.

At some point. The folks on the sidelines will jump back into the market. America is still lacking the inventory we need to house everyone. We’ve talked about this several times. It will take years to build ourselves out of the deficit.

{kind=link}